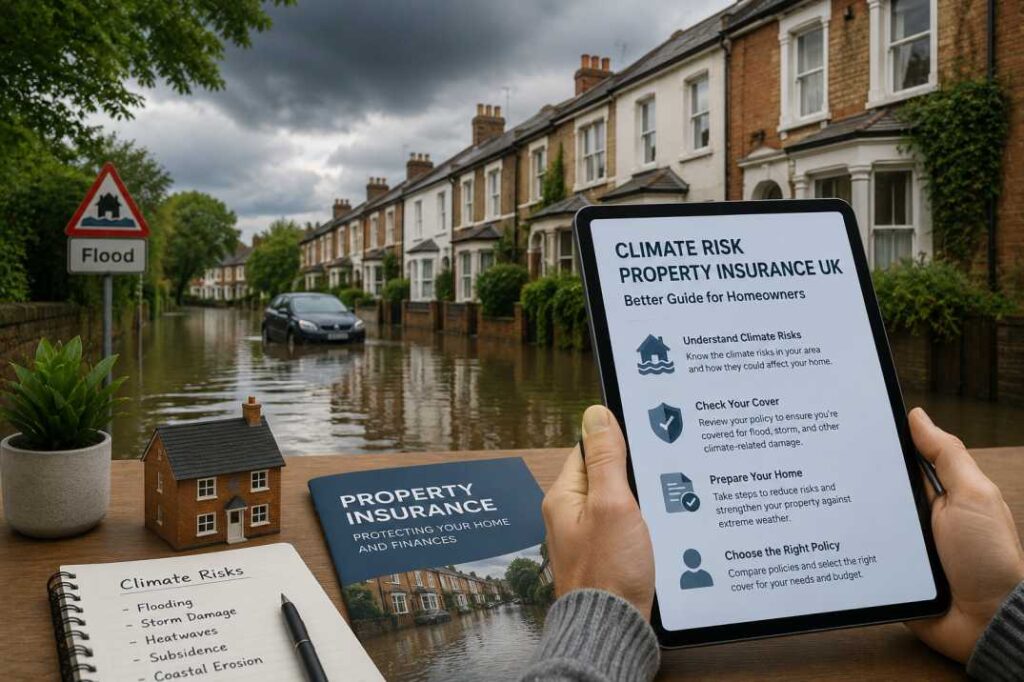

Climate risk property insurance UK is now a serious issue for property developers, lenders, and investors. In some flood-prone areas, cover is harder to buy, more expensive, or full of exclusions. As a result, developers need stronger flood planning before a project starts.

For many schemes, the problem is no longer simple. Standard policies may not be enough. Therefore, developers must combine insurance, resilience design, data, and clear funding plans. This is especially important where uninsurable flood zones property insurance UK concerns affect project value.

Why Flood Zones Are Becoming Harder to Insure

Flood risk is rising in many areas because heavy rain, drainage pressure, and coastal exposure are increasing. Also, insurers now use better climate data. When the expected loss is too high, they may raise prices, limit cover, or leave the market.

Developers can review public flood guidance from the UK Government flood risk service. They can also use the Environment Agency data services to support early site checks.

Main reasons cover becomes difficult

- Repeated flood events in the same location

- Weak local drainage or flood defences

- High repair costs after water damage

- Limited insurer appetite for future losses

- Stricter lender and planning requirements

What This Means for Developers

When insurance is uncertain, the whole project can slow down. For example, lenders may ask for stronger evidence before releasing funds. Buyers may also worry about resale value. Therefore, climate risk property insurance must be part of the business case from day one.

In addition, developers may face higher build costs. However, those costs can protect long-term value. Better drainage, raised services, flood barriers, and resilient materials can reduce damage after a flood.

Blended Risk Transfer: A Smarter Route

Traditional insurance still matters. However, it may need support from other tools. A blended plan spreads risk across different solutions. As a result, developers are not relying on one policy to solve every problem.

1. Parametric insurance

Parametric insurance pays when a set trigger is met. For example, the trigger may be rainfall level, river height, or flood depth. Because payment does not depend on a long damage review, cash can arrive faster.

2. Layered insurance programmes

A layered programme uses more than one insurer or policy. First, a primary policy covers smaller losses. Then, excess or specialist cover can support larger events. This approach can make difficult risks easier to place.

3. Captive insurance

Large developers may use a captive to retain part of the risk. This can reduce reliance on the open market. However, it needs capital, governance, and expert management.

4. Public and private cooperation

Some projects may need support from public flood defence plans. Therefore, developers should understand local authority strategies before buying land. Good local investment can improve the risk profile of a site.

Build Resilience Into the Design

Insurance should not be the only defence. Instead, developers should design buildings that can resist, absorb, and recover from flooding. This makes the project stronger for insurers, lenders, and future owners.

Useful resilience measures

- Raised floor levels and protected utilities

- Flood-resistant walls, floors, and doors

- Permeable paving and better site drainage

- Wetlands, swales, and green infrastructure

- Flood sensors and early warning systems

How AI Supports Climate Risk Decisions

AI can help developers and insurers read large data sets quickly. For example, it can compare rainfall, claims, soil, drainage, and mapping data. As a result, teams can spot risk earlier and price it more clearly.

Also, AI can support claims after a flood. Images, reports, and sensor data can help speed up loss review. Therefore, AI in insurance claims may become more important as climate losses grow.

How to Make a Project More Fundable

Lenders want proof that a site can survive future weather. Therefore, a strong funding pack should explain the risk and the response in plain language.

- Show flood maps and climate risk reports

- Explain all resilience upgrades

- Set out the insurance structure

- Include emergency response planning

- Link the project to net zero and resilience goals

This does not remove all risk. However, it helps lenders see that the project is planned well. It can also support better conversations with insurers.

Future of Climate Risk Property Insurance UK

Climate risk property insurance UK will keep changing as weather patterns shift. Insurers will use more data. Lenders will ask more questions. Developers will need to show stronger resilience before approval.

Meanwhile, new options may grow. Parametric cover, embedded insurance products UK, climate analytics, and net zero insurance strategy work may all play a role. However, the best results will come from combining these tools.

Conclusion

Climate risk property insurance UK is no longer a back-office issue. It now affects land buying, design, funding, sales, and long-term value. Therefore, developers facing uninsurable flood zones need a blended plan.

The strongest approach combines risk transfer, resilient design, clear data, and early lender engagement. With that plan, developers can build safer projects even when flood insurance is difficult.