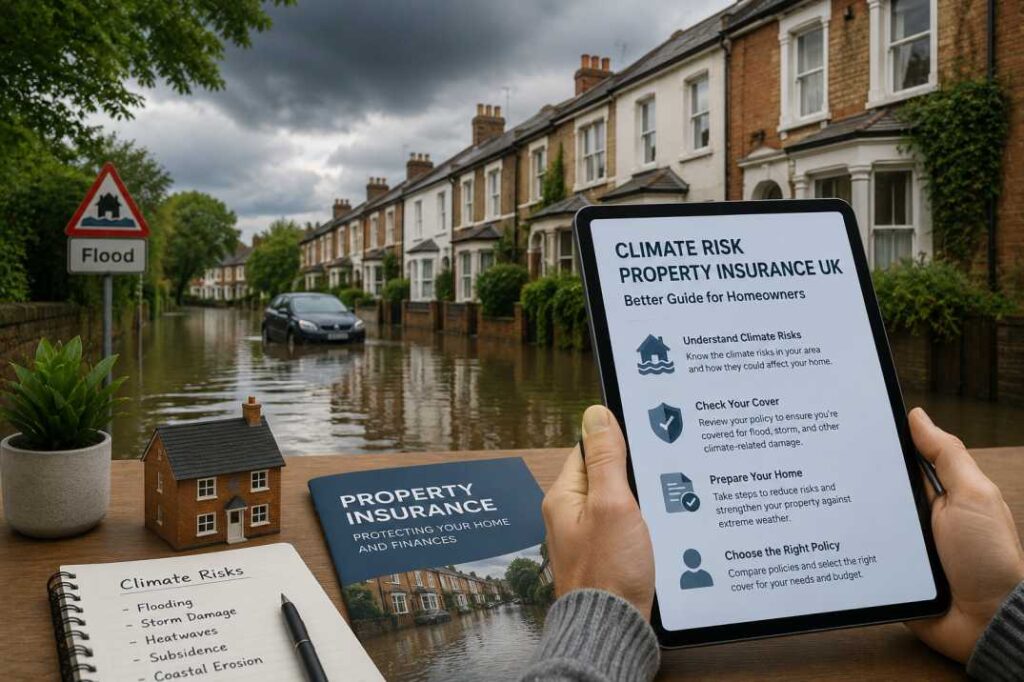

Climate insurance rates are rising because climate change is increasing risks for homeowners. In simple terms, insurers adjust prices as floods, storms, and wildfires become more frequent. Therefore, home insurance is becoming more complex in many regions.

How Climate Insurance Rates Are Affected by Climate Change

Insurance providers calculate risk based on possible damage. Therefore, when climate-related disasters increase, climate insurance rates usually rise as well.

For example, data from the National Oceanic and Atmospheric Administration (NOAA) shows that extreme weather events are increasing. Similarly, the Federal Emergency Management Agency (FEMA) reports higher disaster recovery costs. As a result, insurers raise premiums to manage growing risk. In other words, more risk leads to higher costs. Additionally, this trend is becoming more noticeable year by year.

Main climate risks affecting insurance

- Flooding caused by heavy rainfall and rising sea levels

- Wildfires that damage homes and nearby land

- Stronger storms and hurricanes causing structural damage

- Heatwaves that slowly weaken building materials over time

Key Factors That Influence Climate Insurance Rates

In addition, insurers look at several location and property factors before setting prices. Therefore, your home’s situation plays a major role in your final premium.

For example, location matters a lot. Homes near coasts or wildfire zones often face higher costs. However, homes built with stronger materials may get lower premiums. Furthermore, past claims in your area can also increase rates over time.

| Factor | Impact on Insurance |

|---|---|

| Location | Homes near coasts, rivers, or wildfire zones often face higher premiums |

| Building Materials | Stronger, weather-resistant materials may reduce costs |

| Environmental Exposure | Nearby forests or unstable land increase risk levels |

| Claims History | Areas with frequent past claims often pay more |

Types of Coverage That Affect Climate Insurance Rates

Standard home insurance may not cover every climate risk. Therefore, many homeowners add extra protection for better safety and financial security.

- Flood Insurance: Covers water damage from heavy rain or rising water

- Wildfire Coverage: Helps pay for fire and smoke damage

- Earthquake Insurance: Covers structural damage from seismic activity

For more details on disaster preparedness, you can visit the Insurance Information Institute (III). Additionally, this resource helps homeowners understand coverage options more clearly.

How Homeowners Can Manage Climate Insurance Rates

However, there are still practical ways to reduce long-term costs. For example, improving home resilience can lower risk levels over time.

In addition, small upgrades can make a big difference. For instance, better drainage systems can reduce flood damage. Likewise, stronger roofing can reduce storm-related losses. As a result, insurers may offer better pricing over time.

- Upgrade roofing and strengthen structures

- Install better drainage or flood barriers

- Use weather-resistant building materials

- Bundle insurance policies for discounts

- Compare providers regularly for better pricing

Final Thoughts on Climate Insurance Rates

In conclusion, climate risk insurance rates are directly influenced by climate change and rising disaster risks. However, homeowners can still take smart steps to reduce exposure and manage costs over time.

By staying informed and proactive, you can better understand how climate risks affect insurance pricing. Therefore, you can make more confident decisions about protecting your home.