AI exclusions insurance language is becoming a major issue during commercial policy renewals. As businesses use artificial intelligence for claims support, marketing, analytics, customer service, and pricing, insurers are adding new exclusions and endorsements that may limit coverage.

Because of these changes, agents and brokers should no longer assume last year’s policy wording still applies. Moreover, In many cases, one small endorsement or vague AI exclusions insurance clause can create a serious coverage gap after a claim.

Therefore, every renewal should include a careful review of definitions, exclusions, cyber wording, endorsements, and professional liability terms. A proactive review process can help clients avoid unexpected disputes later.

Why AI Exclusions Insurance Language Is Expanding

AI Exclusion Insurers are trying to manage emerging risks linked to artificial intelligence. Since AI-related exposures continue to evolve, many carriers are tightening policy wording to reduce uncertain claim costs.

For example, AI-related claims may involve:

- Incorrect automated advice

- Bias or discrimination allegations

- Privacy and data misuse claims

- Deepfake fraud incidents

- Copyright and trademark disputes

- AI-assisted cyberattacks

- Errors caused by automated systems

At the same time, regulators are increasing oversight of AI use. Agents can review updates from the National Association of Insurance Commissioners and the Federal Trade Commission for broader guidance on evolving risk issues.

What Is an AI Exclusions Clause?

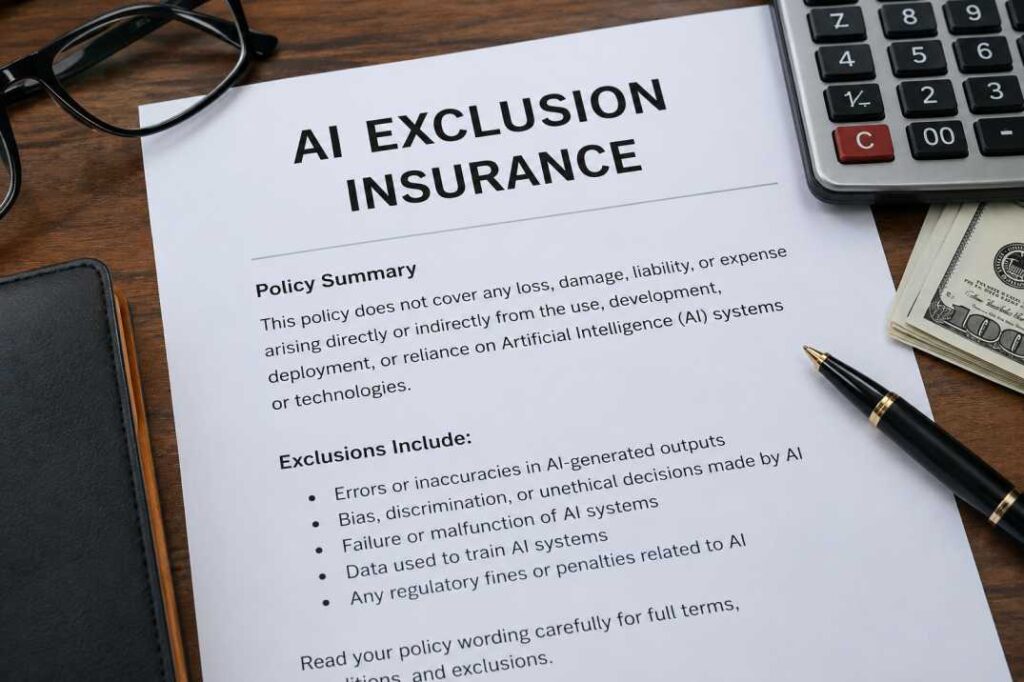

An AI exclusions clause is policy wording that removes or limits coverage for claims involving artificial intelligence, machine learning, automated decisions, or AI-generated output.

However, not every exclusion works the same way. Some are narrow and specific, while others may apply broadly to common business software and automated systems.

Common AI Exclusion Examples

- Claims involving automated decision systems

- AI-generated recommendations or advice

- Copyright disputes tied to generative AI content

- Bias or discrimination claims linked to algorithms

- Cyber losses involving AI-enabled attacks

- Technology E&O claims tied to machine learning failures

As a result, agents should compare renewal wording against the expiring policy line by line instead of relying on summaries alone.

Policy Language Red Flags Agents Should Watch

1. Broad Definitions of Artificial Intelligence

Some policies define artificial intelligence very broadly. For example, wording may include terms such as “automated processing,” “algorithmic systems,” or “machine-assisted decisions.”

Consequently, the exclusion could affect ordinary software tools instead of only advanced AI applications.

2. Undefined Technology Terms

Vague technology wording often creates confusion during claims handling. Agents should pay attention to terms such as:

- Autonomous systems

- Machine-generated output

- Predictive analytics

- Synthetic media

- Adaptive software

If the wording is unclear, agents should request written clarification from the underwriter before binding coverage.

3. Hidden Endorsements at Renewal

Many insureds focus only on premiums and declarations pages. However, important AI exclusions insurance changes often appear inside endorsements added at renewal.

Because of this, agents should review the complete endorsement schedule and explain significant changes in writing.

4. Cyber Wording That Avoids the Term AI

Some cyber policies limit AI-related losses without directly using the term “AI.” Instead, exclusions may reference synthetic communications, automated network activity, or self-learning malware.

As a result, clients may incorrectly assume AI-related cyber risks remain fully covered.

5. Professional Liability Restrictions

Professional AI liability policies may limit coverage when businesses rely on AI-generated advice or automated recommendations. This issue can affect consultants, accountants, healthcare providers, marketers, financial advisors, and legal service firms.

Therefore, agents should ask how clients use AI in reports, pricing, recommendations, or customer decisions.

6. Generative AI and Intellectual Property Limits

Generative AI tools can produce content, images, code, and marketing materials quickly. Nevertheless, they can also create copyright and trademark concerns.

For that reason, agents should review whether cyber, media liability, or technology E&O policies exclude AI-generated content claims.

Industries With Higher AI Exclusion Risk

Some industries face greater exposure because they depend heavily on automation and AI-assisted workflows. Therefore, these businesses should receive closer policy reviews.

Technology Companies

SaaS providers, software developers, and AI startups face elevated risk because automated systems may directly affect customer operations.

Healthcare Providers

AI-assisted diagnostics, patient support tools, and scheduling systems may create privacy, compliance, or malpractice concerns.

Financial Services Firms

Automated lending, underwriting, and investment systems can increase professional liability and regulatory exposure.

E-Commerce Businesses

Online retailers often rely on recommendation engines, fraud tools, and AI chatbots. Consequently, they should review both cyber and consumer protection coverage carefully.

Marketing and Media Agencies

Agencies using AI-generated images, copy, or videos should review media liability and intellectual property wording in detail.

How Agents Can Reduce Coverage Gaps

Review Renewals Carefully

First, compare renewal wording with the expiring policy. Even one additional endorsement may significantly narrow coverage.

Ask Clear Underwriting Questions

Next, ask carriers how they interpret vague AI-related wording. Written clarification can help reduce future disputes.

Negotiate Narrower Exclusions

In some situations, insurers may agree to revised wording. For example, agents may request:

- Exclusions limited to specific AI activities

- Defense cost carve-backs

- Coverage for third-party claims

- Sublimits instead of complete exclusions

- Separate endorsements for high-risk exposures

Document Client Discussions

Agents should document conversations about AI use and policy changes. This process creates a clearer record of what was reviewed and explained.

Consider Supplemental Coverage

Finally, some businesses may need additional protection through cyber liability, media liability, technology E&O, or specialized AI endorsements.

Questions Agents Should Ask Clients

Many businesses use AI tools without realizing the insurance impact. Therefore, agents should ask practical renewal questions such as:

- Do you use generative AI tools?

- Do AI systems make decisions without human review?

- Does AI influence customer advice or pricing?

- Do you rely on third-party AI vendors?

- Do AI systems handle sensitive customer data?

- can you use AI for fraud detection or cybersecurity?

- Do employees create AI-generated content or code?

These questions can help identify hidden exposures before claims arise.

What Buyers Should Review Before Renewal

Business owners should review more than just policy summaries. Instead, they should examine the full policy with their broker or agent.

Important sections include:

- Definitions

- Endorsements

- Cyber exclusions

- Professional liability wording

- Intellectual property exclusions

- Technology E&O provisions

- Defense cost carve-backs

In addition, buyers should clearly explain how their company uses AI systems each day. Better disclosure often leads to more productive coverage discussions.

Final Thoughts on AI Exclusions Insurance

AI exclusions insurance wording is changing the way commercial policies are reviewed and negotiated. One broad AI exclusions clause may affect claims involving cyber events, automated advice, privacy issues, intellectual property disputes, or AI-generated content.

Therefore, agents should review renewals carefully, ask better underwriting questions, and negotiate narrower exclusions whenever possible. With a structured review process, businesses can reduce costly coverage gaps and make more informed insurance decisions.